Elvira Nabiullina

and Saving Russia’s Financial System

Elvira Nabiullina is currently ranked the most powerful woman in Russia and has been named one of the world’s most effective Central Bank heads. Through her stewardship of Russia’s Central Bank, Russia has been able to steer through the Russian financial crisis of 2014.

When she was appointed, the forces of that crisis were just beginning to gather. These forces, at their most powerful, included mounting corporate debt, plummeting oil prices, budget constraints, a troubled banking sector, Western sanctions, Russian counter-sanctions, a rapidly devaluing ruble, and escalating inflation all occurring within a global economic downturn. Nabiullina’s solutions to these complex problems have been market-based, in keeping with her generally liberal economic philosophy. Russia still faces big challenges and not all of the forces have abated. However, Bank of America has recently declared Russia the most stable emerging economy in the world with Russian inflation at its lowest levels since the fall of the USSR. Unemployment also remains low, and wages are beginning to increase as well.

Oil and gas account for around 50% of the Russia state’s revenues. The steep plunge that oil prices took in 2014 played havoc with Russia’s budget and economy. Graph from Nasdaq.com.

The “perfect storm” of 2014 could have caused much more severe damage to Russia’s economic and even political system. Nabuillina’s ability to successfully implement bold and effective solutions in the face of significant opposition has shown her to be one of the most powerful members of the “liberal camp” within the Russian government. Her name has even been floated in discussions regarding a potential replacement for Putin should he chose to retire.

Background, Education and Early Career

Elvira Nabiullina was born on October 29, 1963 in the city of Ufa, in Russia’s southern Urals. Her family is Tatar, Russia’s largest ethnic minority. Her father was, by profession, a chauffeur and her mother worked in a local factory. Nabiullina graduated from secondary school in Ufa with perfect marks and went on to graduate with a Specialist’s Degree (the equivalent of a Master’s) in Economics from Moscow State University in 1986.

A 2011 photo of Nabiullina with now-Moscow Mayer Sergey Sobyanin. Nabiullina, a small woman, often comes across in interviews as unassuming, quiet, and charming but also direct and confident.

She remained at Moscow State for another four years pursuing a doctorate. However, she never defended her dissertation despite completing it and later publishing her work. She has never publicly offered an explanation for this episode.

Nabiullina’s first job out of graduate school was for the Union of Science and Industry, where she was named a Chief Specialist in 1991. After the Soviet Union collapsed later that year, the Union was renamed the Russian Union of Industrialists and Entrepreneurs (RSPP). She continued on as a consultant on economic policy. The RSPP remains large and influential today.

Nabiullina left the RSPP in 1994 to become Deputy Head of the Department of Economic Reform under the Russian Ministry of Economy, where she tackled questions surrounding Russia’s market liberalization programs. In 1996, she was promoted to head the department and a year later, promoted to Deputy Minister.

Despite her rising star, Nabiullina has expressed reservations about her work at the Ministry. Although she found the economic reforms of the 90s necessary – including the rapid creation of a “class of private owners,” she also criticized the implementation of these reforms as generating:

an atmosphere of distrust toward private property…It is a problem that has haunted us for many, many years. Because respect for private property, respect for the entrepreneur – is the most important component of the market economy.

The reforms of the 1990s created chaos, which resulted in mass emigration and a sudden drop in life expectancy as people lost jobs, crime escalated, health care collapsed, and drug and alcohol abuse became much more prominent. Recent trends have been positive, however.

Ultimately, the reforms did create a propertied class. However, they also created massive poverty, rising crime, and social disruption. Nabiullina left the Ministry in 1998 and served in a range of private sector jobs for two years: Deputy Chairwoman of Promtorgbank, a relatively successful bank servicing industrial companies, and Executive Director of the Eurasian Rating Agency. She then took the position of Vice President at the newly-formed Center for Strategic Research, an economics-based political policy think tank formed to advise Vladimir Putin, who was then running in his first campaign in a Russian presidential election. The Center developed what became known as Strategy 2010, a set of reforms designed to repair the damage of the crises of the 1990s and return Russia to stable development.

Return to Government and Rise to Prominence

When Putin was elected president, most of those who had worked on Strategy 2010 moved to the government to oversee its implementation. The head of the Center, Herman Gref, a noted liberal-minded reformer, became the head of the newly-reformed Ministry of Economic Development and Trade. Nabiullina served as First Deputy Minister at the Ministry from 2000 to 2003. During this period, Nabiullina was highly instrumental in implementing reforms to drastically lower inflation and improve Russia’s economic environment.

From 2003 until 2007, she returned to the Center for Strategic Research as its head. The Center remained in direct connection with Putin and influential in creating policy directions for Russia. In 2005, she also chaired the organizing committee tasked with preparing Russia’s highly visible 2006 G8 presidency. The following year, she was selected by Yale University as one of 18 “emerging leaders” to participate in its World Fellows program.

Nabiullina and her early mentor, German Gref, now the CEO of Sberbank, one of Russia’s largest banks.

In 2007, Herman Gref stepped down as Minister to head Sberbank, Russia’s largest private bank. Nabiullina replaced him as Minister of Economic Development and Trade. During her tenure, she frequently clashed with Finance Minister Alexei Kudrin. Kudrin, for his part, sought to address Russia’s rising budget deficit by raising taxes and increasing the retirement age. Nabiullina argued for an expanded tax base and more efficient government investment to spur growth. Kudrin’s suggestions lost in the end. He was eventually forced from his position over his opposition to military rearmament.

While Minister of Economic Development and Trade, Nabiullina also worked in several other roles which allowed her to implement policy directly through state-owned firms and state-supported projects. A short list of these endeavors include: member of the Supervisory Board of Rostek, a state-owned holding company created to advance the “development, production, and export” of Russian industrial goods (2007-2012); member of the Board of Directors of natural gas giant Gazprom (2008-2011); member of the Government Commission to address Economic Development and Integration; and member of the Board of Trustees of the Skolkovo Foundation, a non-profit geared towards sustainable development and innovation (2010-current), among several others.

Despite major fluctuations in the ruble’s relative value, state revenues, and other major factors, inflation has been aggressively targeted by Nabiullina’s policies and is set to hit a post-Soviet low in 2017. Chart from TradingEconomics.com

Following Putin’s reelection to the presidency in 2012, Nabiulina was appointed his Special Economic Advisor, working directly with the president.

The Central Bank and the 2014 Crisis

Nabiullina’s 2013 candidacy to head Russia’s Central Bank was both praised and criticized. Some noted her close relationship with Putin as a considerable hindrance to her ability to act independently. The Central Bank, according to the Russian Constitution, must be independent of the Russian presidency and legislature. Moreover, Nabiullina’s top-down management style was criticized as not allowing for diverse views among her subordinates. Others defended the effectiveness of her methods and stressed that she speaks her own views openly even if they conflict with the status quo. In any event, all parties agree that Nabiullina was in many ways a “compromise candidate”—occupying a middle road between conservative and liberal economists.

Nabiullina has typically shied from questions of political ideology, often treading a middle path. Although described by university classmates as exceptionally passionate about Communist ideals when she joined the Communist Party in 1985—even receiving honors from Communist organizations—while serving in government she consistently championed market-based solutions to Russia’s economic woes. Nonetheless, she maintains the view that the state can function as a legitimate investor in the economy.

Elvira Nabiullina speaks to Bloomberg News as her 2014 changes to monetary policy take hold.

The major origins of the 2014 crisis lie in the 2007-2008 global financial crisis when many Western states, including the US, lowered interest rates to 0%. Global investors thus sought opportunities in the higher interest rates offered by the developing world, including Russia. Russian companies accepted these funds, issuing bonds and accepting loans in foreign currencies. This was considered safe because the Russian Central Bank, by policy, made market interventions anytime the ruble exchange rate went under or over a narrow band for a basket of world currencies. This practice originated while Russia was accepting World Bank financing during the 1990s, both as a condition for financing and as a way to ensure that Russia’s ruble-based economy would be able to pay back loans made in currencies other than rubles. The policy continued ever since, largely as a way to ensure credit ratings and stability.

In 2014, the world supply of oil boomed as a consequence of new technologies, and the price crashed. Russian state income, heavily reliant on oil exports, plummeted. This effect, in turn, vastly increased pressure on the Russian ruble as speculators, predicting that oil would crash the Russian economy, bet against the ruble en masse.

Nabiullina elected to solve both problems by allowing the ruble to float at its true market value. The idea had been long debated. Although not without risk, a weakened ruble was predicted to improve the competitiveness of Russian industry by making Russian products cheaper on world markets. Moreover, most analysts also agreed that Russia’s currency had been held artificially high by the former policy and that pressures on it were neglected because investors were confident that the state would continually fund the ruble to maintain its stability. This environment, of course, changed when the state’s ability to fund such an effort became seriously questioned.

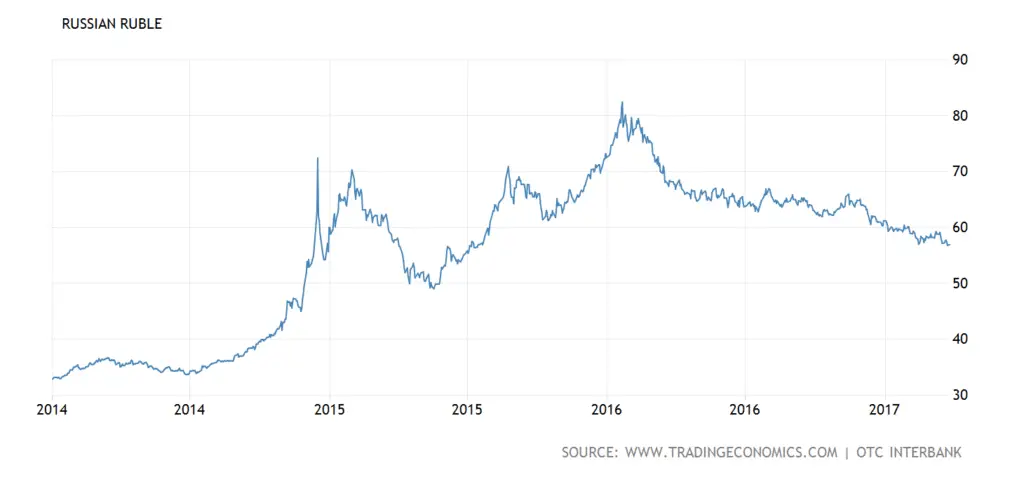

The massive fluctuation in the value of the ruble came in part from the fall in oil prices but mostly from Nabiullina’s decision to end state support for the ruble in later 2014. Chart from TradingEconomics.com

Further, allowing the ruble to float freed up more rubles for the Russian government to spend on social programs and spending programs. It also meant that each barrel of oil sold for dollars on the Russian market brought more rubles into Russia as each dollar came to purchase more rubles inside Russia. This has been consistently named as having been instrumental in helping Russia maintain its budget during the crisis.

Nabiullina’s decision to float the ruble led to other problems. Rising exchange rates meant that imported items, on which Russia is dependent, rose in value, driving inflation up to as much as 16%. In addition, it meant that the debt burden faced by Russian companies and individuals holding debt denominated in foreign currencies increased, creating further inflationary pressure as demand for rubles to pay back foreign currency loans grew. Pressures mounted after Russia annexed Crimea and Western sanctions created further economic uncertainty by restricting investment and loan opportunities. Russian agricultural counter-sanctions only exacerbated the problems, disrupting supply lines and driving up the cost of many food items.

To combat rapid inflation, Nabiullina boosted Central Bank interest rates to 17%, drawing in deposits both domestically and internationally and directing these funds to refinance foreign currency loans. The market also helped correct itself, with Russian suppliers, for instance, replacing imports of American beef with Brazilian beef, where the exchange rate was more favorable. In addition, higher prices and government programs encouraged investment in Russia’s food industry, bringing down prices by localizing production.

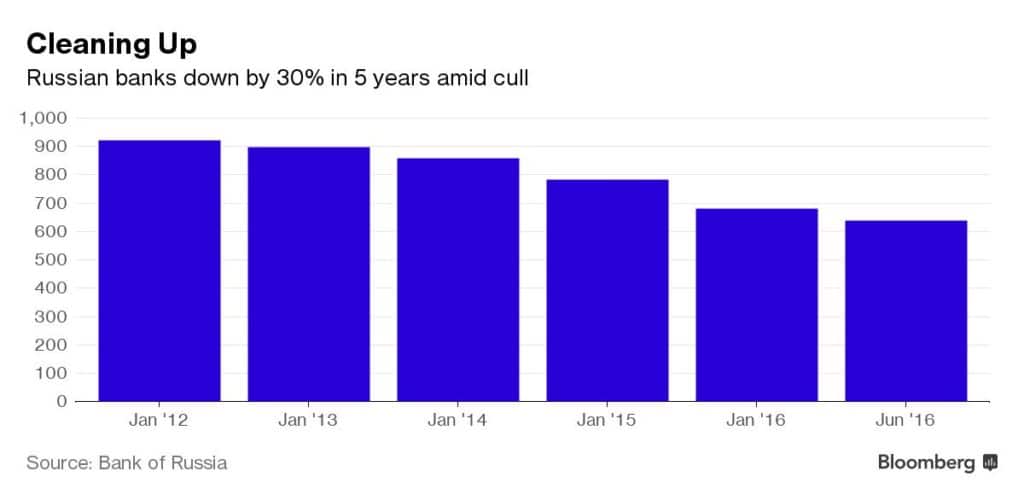

Nabiullina also co-opted the instability of the banking sector, aggressively and methodically shuttering institutions that were deemed at-risk, under-capitalized, or in use of corrupt banking practices. The liquidation or merger of these institutions was both announced and controlled by the Central Bank and supported by Russia’s National Depositors’ Insurance. This helped minimize bank runs and to consolidate the industry around fewer, healthier banks.

Nabiullina has aggressively closed under-capitalized banks and those operating under questionable practices.

Nabiullina’s methods were heavily debated. For most of the public, volatile food prices and short-term shortages of some items were constant and concerning reminders of exchange rate volatility. For Russia’s middle class, the loss of imported foods and restrictions on their ability to travel to European vacation spots was also an irritant. Many members of Russia’s political opposition argued that the government intervention was too heavy.

On the other hand, many government officials also argued that the intervention was not heavy enough. Then-Economic Minister Alexei Ulyukayev argued for a 140 billion ruble stimulus to the banking sector to improve lending to businesses. Nabiullina countered that this move would negatively impact her inflationary controls. Sergei Glavyev, who is currently Special Economic Advisor to the president, sharply denounced Nabiullina for her interest rate policy, her refusal to implement formal capital controls, and for her decision to float the ruble. He also labeled her policies as a return to the “shock therapy” of the 1990s and instead stressed a more Keynesian style stimulus spending to encourage growth. In the end, however, Nabiullina won nearly every policy fight.

Although often unassuming, Nabiullina can also be sharp and demanding in official meetings.

It can be argued that Nabiullina’s very public decision making and her ability to take bold but also moderate measures allowed Russia to maintain an economic environment in which neither the public nor investors fully panicked. In January of 2016, most Russians still felt that the government was in control of economic forces. While there was a consumer spending spree as volatility set in, there were no bank runs nor was there any major disorder in Russian retail establishments. In this way, consumer spending appears as a much more calculated investment move—with Russians spending rubles before they dropped in value and before prices rose—rather than a “panic” as it has been often called in the English-language press. Moreover, investors have praised Nabiullina’s policies.

Arguably the biggest figure that Nabiullina has taken on is Igor Sechin, who has long been a powerful force in the Russian government and state companies and who is currently the head of oil company Rosneft. Nabiullina “publicly chided” him for selling off bonds to deal with his company’s debt, arguing that Rosneft’s massive economic weight was endangering the ruble and Central Bank policy. Sechin requested a private meeting and, after a closed-door session, complied with the Central Bank so as “not to appear to be manipulating the national currency.”

However harsh her methods, Nabiullina has managed to stabilize the economy and win praise from many international economists for her unwillingness to bend under pressure and for her apparent foresight. Russia’s economy still faces a host of challenges in the short and long terms and many specialists—including Nabiullina herself—worry that a secondary recession may be unavoidable without a large boost in investment. After two years of recession and at least another year of near-stagnation, Russians are also beginning to lose faith that the government really has things under control. Yet, it seems clear that Nabiullina is committed to restructuring the Russian economy, making it less dependent on state intervention and oil revenues. Her policies have continued to maintain stability under adverse conditions and to keep inflation low. Her ability to take on Russian political heavyweights and the apparent trust placed in her by Putin, all point to her continuing to play a very visible and influential role in the Russian government.